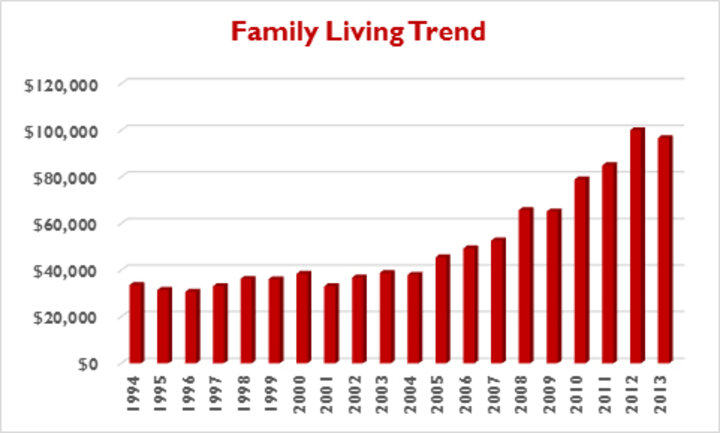

Figure 1. Family living expenses 1994-2013 for a group of Nebraska farmers and ranchers participating in the Nebraska Farm Business, Inc.

Figure 1 shows the total cost for the past 20 years of family living for a group of Nebraska farmers and ranchers I work with through the Nebraska Farm Business, Inc. This cost includes all cash costs for living, but does not include non-farm investments, savings, or non-farm capital purchases (houses, vehicles, etc).It doesn't take an expert to see the dramatic increase in the amount of money spent on family living from just about $34,000 in 1994 to almost $100,000 in 2013. Family living expense actually held pretty steady through 2004 and then there was a persistent increase each year. So what happened? It's not surprising that 2004 was also the first of 10 years of record high net farm income. When farm income went up, family living followed right behind it. So what will happen when farm income goes down?

Looking Forward

In 2013, the average net farm income fell to the lowest point we've seen since 2005 and we expect average net farm income to fall even further in 2014 due to low crop prices and high input costs. With rapidly declining incomes, how do we start to control runaway family living expenses? I often hear that the increase must be coming from medical costs, education, and other things we have little control over. The reality is those are certainly increasing costs, but like farm costs, it is really an increase in every little expense that leads to a huge difference. The table shows the breakdown of expenses and the difference between costs in 2004 and 2013.

|

|

2004 |

2013 |

Difference |

|

Food |

$5,690 |

$10,069 |

$4,379 |

|

Medical Care |

$4,580 |

$6,699 |

$2,119 |

|

Health Insurance |

$3,698 |

$6,996 |

$3,298 |

|

Cash Donations |

$2,131 |

$5,130 |

$2,999 |

|

Household Supplies |

$1,739 |

$7,078 |

$5,339 |

|

Clothing |

$1,695 |

$4,119 |

$2,424 |

|

Personal Care |

$1,921 |

$7,471 |

$5,550 |

|

Child/Dependent Care |

$509 |

$1,293 |

$784 |

|

Alimony/Child Support |

$77 |

$0 |

$-77 |

|

Gifts |

$1,940 |

$4,674 |

$2,734 |

|

Education |

$1,713 |

$3,327 |

$1,614 |

|

Recreation |

$1,776 |

$9,081 |

$7,305 |

|

Utilities |

$2,037 |

$2,952 |

$915 |

|

Personal Auto |

$2,365 |

$4,185 |

$1,820 |

|

Household Real Estate Taxes |

$196 |

$1,372 |

$1,176 |

|

Dwelling Rent |

$227 |

$514 |

$287 |

|

Household Repairs |

$2,285 |

$3,529 |

$1,244 |

|

Personal Interest |

$881 |

$1,909 |

$1,028 |

|

Disability/Long Term Care Insurance |

$263 |

$612 |

$349 |

|

Life Insurance Payments |

$3,002 |

$5,606 |

$2,604 |

|

Personal Property Insurance |

$176 |

$175 |

$-1 |

|

Miscellaneous |

$6,059 |

$9,979 |

$3,920 |

|

Total |

$44,644 |

$96,680 |

$52,036 |

|

|

|

|

|

|

Income Taxes |

$7,840 |

$56,269 |

$48,429 |

|

Non-Farm Capital Purchases |

$7,243 |

$43,472 |

$36,229 |

|

Non-Farm Savings |

$2,392 |

$11,357 |

$8,965 |

|

Total Non-Farm Expenses |

$62,119 |

$207,778 |

$145,659 |

The 2013 bottom line of $207,778 coming out of the farm for non-farm purposes is a staggering number. The reality is that number is going to have to come down and come down fast to avoid significant net worth losses in the coming years. A farm can be profitable and still have a net worth loss if the non-farm costs are higher than the income (farm and non-farm combined).

How do you begin to reduce this expense?

Like farm costs, each non-farm cost must be evaluated all year long. It is too late to sit down at the end of the year and be amazed at how much money has gone out the door. If you're at a loss for where to start, compare your family living costs to these averages. I know that a massive red flag that would be flying if I did this with our family's costs would be Food and Meals. With two working parents, four active kids and 10 restaurants between work and home, it is hard to keep our family out of restaurants and eating at home. This keeps our food and meal expense well above average.

Knowing your problem and controlling it are two different things. To reduce our eating out, we would have to make hard lifestyle changes. We may have to:

- give up on having all six of us eat together,

- cut back on the activities the kids are involved in, or

- cut back hours at work to have more time for grocery shopping and preparing meals.

No one else can make these decisions for our family any more than I can make those decisions for another family. Just like farm expenses, it takes discipline to reduce non-farm expenses. It is just as hard to cut back on vacations as it is to reduce the extra amount paid for cell phones and cable bills.

The Difference 10 Years Can Make

There are so many things that we take for granted today that we never considered in 2004. I know our family had one cell phone that we shared that probably cost us $35 per month. I would have laughed to even think that my kids would have cell phones before they could drive, but we have turned that one dumb phone expense into monthly payments for four smart phones. I now can't imagine how our lives would work without that constant connection. There are other things like the DVR, high definition, high-speed internet, and vehicles with Wi-Fi, Amazon, and iTunes that have changed the way we live and the way we spend our money.

No matter the differences between then and now, there is a limited amount of money available to spend. For those receiving a wage, it is easy to see how much money can be spent each month. When there's an operating note available, it's easier to let that spending get out of hand. Each individual family is going to have to make their own choices as to what is important for them to spend their money on.

Living like the Jones, and the Smiths, and the Johnsons

This article is the third in a series by Tina Barrett focusing on farm profitability despite low commodity prices. Watch for more Belt Tightening on a variety of topics this fall and winter. Also see:

Clients often bring up what their neighbors are doing and "Why can't we afford that?"

"The Jones went on a three-week cruise this summer."

"The Smiths built a new house."

"The Johnsons have a new Escalade."

"The Andersons bought a lake house."

What we don't know is whether these families have been saving up for years for these extra things. We don't know if the Johnsons haven't taken a vacation in 10 years as they would prefer to travel to town in comfort every day instead. We don't know if the Smiths received an inheritance from a long-lost uncle with the money to build that new house. We don't know if the Anderson's purchase was financed and may be the final straw that keeps them from making their loan payments and leads to being forced to have a farm sale next year. We can only control our own costs and make the allocations of what we can afford for ourselves.

If you can't find ways to cut family living and there's no way to increase farm income, the other choice is to find non-farm income to supplement the spending. Everyone will eventually have to find a way to balance the money going out with the money coming in.