On Tuesday, Dec. 16, the Senate passed a bill to extend several tax provisions that had expired on Jan. 1, 2014. The House had passed the bill on December 3 and we are still waiting for the promised signature of President Obama. The extension would be through Dec. 31, 2014.

Depreciation Changes

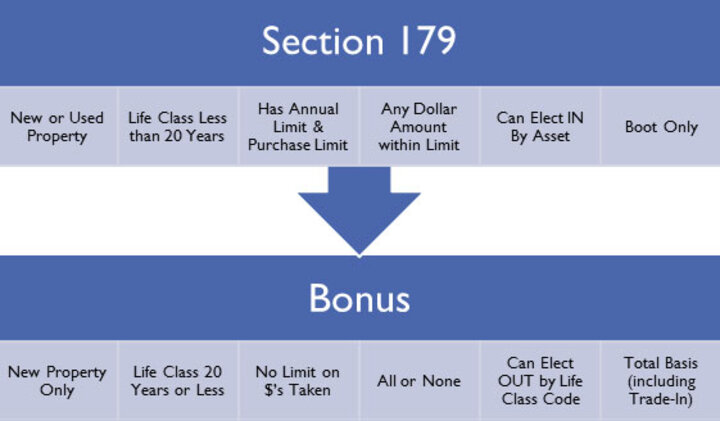

One of the major changes that applies to farmers is the extension of the enhanced levels of Section 179 expense election and bonus depreciation. These are both provisions to increase the speed at which capital items can be depreciated, but they are very different in what type of assets qualify for each.

Section 179

Section 179 allows the full write-off of most assets in the year of purchase by individuals in an active trade or business (not cash rent landlords). Assets must :

- have a life class of less than 20 years,

- be tangible personal property, and

- not have been purchased from a related party.

Most farm assets qualify for Section 179 including tractors, combines, cows, and pickups (over 6,000 lb gross vehicle weight). Each tax return can only use $500,000 of section 179 expense in a tax year and your total qualified purchases cannot exceed $2 million. The election is now available for all 2014 tax returns, regardless of filing deadlines.

Bonus Depreciation

Bonus depreciation allows for a 50% write-off for assets purchased between January 1and December 31, 2014 (regardless of fiscal tax year). The assets must be brand new (first use) and have a life class of 20 years or less.

Deduction Differences

The major difference between what qualifies for the types of deductions is farm buildings. With a life class of 20 years, they qualify for bonus depreciation but not Section 179. We also have to be careful with the designation of "new" assets as used assets qualify for Section 179.

Also, you must elect out of Bonus Depreciation and you have to elect out by life class, which means you cannot take a bonus depreciation on a tractor but not on a combine (assuming they're both new) since they are both in the seven-year life class. Bonus is available to more taxpayers as you do not have to have an active trade or business which means cash rent landlords can take advantage of bonus depreciation.

The chart explains a few of the differences between the two accelerated depreciation types.

We only have two weeks before this law expires again. No provisions were made for 2015 so at this point we are back to waiting for Congress to act to prevent elimination of the bonus depreciation and the Section 179 limits to return to $25,000 expense limit and a $200,000 purchase limit in 2015.

If you have any questions about this and how it affects your tax plan, contact your tax professional.

Tina Barrett

Executive Director, Farm Business Inc.

UNL Department of Agricultural Economics