The 2017 averages from farm and ranch operations serviced by Nebraska Farm Business, Inc. were recently released. These averages represent 119 farms across the state participating in this financial management program.

Each year the data collected from these farm records is averaged to provide participants with information to benchmark their operations. Taking a closer look at these averages also indicates shifting trends across these farms and ranches.

This was the fifth consecutive year with lower accrual net farm incomes. This year’s numbers were lower than in the previous eight years. While the downturn in the agricultural economy was not expected to be resolved quickly, the lower incomes have continued to put financial stress on many operations. The good news is that average incomes in Nebraska were higher in 2017 than in 2015 and 2016, and there was a slightly positive increase in net worth for the first time since 2014.

As we dig deeper into the data, we see that crop operations (those that receive more than 70% of their net farm income from the sale of crops) actually saw a 20% decline in net farm income from 2016 to 2017 while operations with a heavy beef influence saw significant increases in net farm income. Those increases were significant enough to cause the average income overall to be higher.

Financial Stress Showing

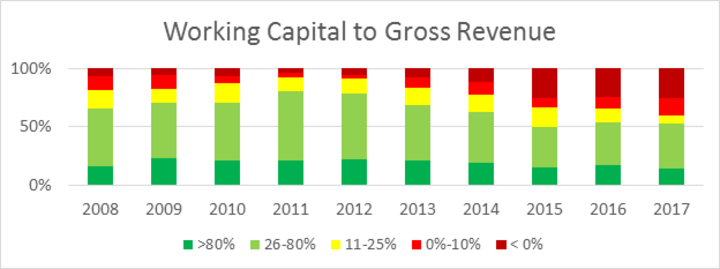

The financial stress is showing most significantly in the Working-Capital-to-Gross-Revenue Ratio. This ratio is one of three liquidity ratios that measures an operation’s ability to pay their obligations in the next 12 months. In other words, do they have enough stuff to sell to make the payments they’ve committed to in the next 12 months? Figure 1 shows the distribution of farms in each of the categories.

When we talk about ratios, we often use a stoplight analogy. Farms in the “red” categories are not in a healthy position. The “yellow” category means caution is needed, and the “green” categories mean they’re good to go. You can see from the trend that we are really “squeezing” the number of farms in the yellow which tells me we are seeing a divided trend of about half the operations doing well and the other half in cash flow trouble. The farms in the red category are not necessarily the same operations each year. In reality, we have seen a lot of refinancing done in the past few years that moves current debt to the long-term position. This refinancing would move an operation from the “red” to the “green;” however, for every operation we have moved out of the “red,” another seems ready to take its place.

The longer-term ratio, Debt-to-Asset, shows the same “squeeze” of the yellow category with more farms moving to a ratio exceeding 80%. This trend is more alarming than the Working-Capital-to-Gross-Revenue ratio because there is no “easy fix,” like refinancing to improve the number.

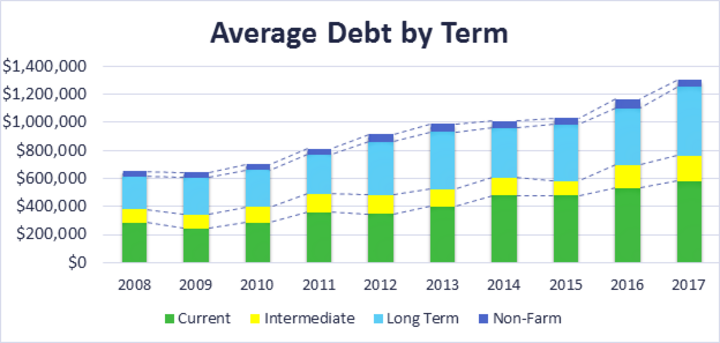

Another measure we have been watching closely is the ever-increasing level of total debt (Figure 2). Every year since 2009 has seen a fairly significant increase in the average amount of total debt. This year was no exception, with debt climbing to over $1.3 million per operation on average. The largest increase was in the long-term position. It seems this is a reflection of the refinancing of current debt more than asset acquisition, given the average amount spent on buying farm land was down from 2016 and was half of the average increase in long-term debt.

Family Living

After the first significant decline in family living expense in 2016, the costs resurged in 2017 to within $700 of the highest year on record. A major contributor to the increase in family living cost was health care. The combined increase between Medical Care and Health Insurance categories was almost $3,000 or 18.5% of the increase. Recreation and Miscellaneous Expense categories contributed to over one-third of the total increase.

We saw a decrease in Non-Farm Capital Purchases as well as Income and Social Security Taxes which kept the total amount of Non-Farm Costs about the same as in 2016.

Cost of Production

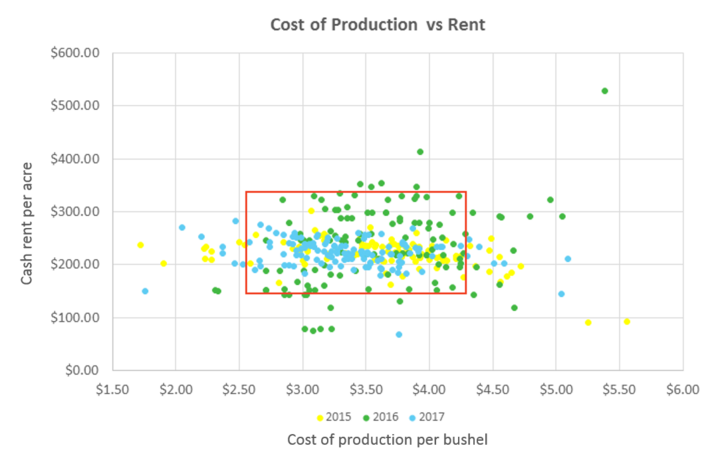

Figure 3 shows three years of cost of production. Each dot represents one farm’s cost of production for Irrigated Corn on Cash Rented ground. While the chart can look pretty busy, the cost of production in 2017 was much more concentrated than in the past two years. This shows that the extreme cash rents are coming down to a more reasonable rate. The chart also shows more blue dots to the left than in the past, which means more operations are making an adjustment to a lower cost of production. It’s always important to remember that cost of production is not only made up of costs but also production. While 2017 saw extreme wind events over much of the state during harvest, these numbers are not showing anything too dramatic.

Summary

The division in the financial health of the operations included in these averages is concerning. Certainly some operations have made adjustments to the economic downturn and will not only survive but continue to thrive through these tougher times. On the other hand, there seem to be a growing number of operations that have not adapted and continue to struggle. Time will tell if they have enough equity to withstand this downturn, or if we will start to see a gradual increase in the number of operations exiting from the industry.

A full report of this data is available for purchase from our website, www.nfbi.net. Look under Farm Analysis – Annual Reports.