Sept. 5, 2014

The prices of agricultural commodities are ultimately dictated by supply and demand. Increased corn supply from US growers places downward pressure on corn prices. Corn prices can also respond by incentivizing storage, increasing net corn price received, and improving financial standing. The purpose of this article is to describe the decision-making environment for marketing the 2014 corn harvest.

Understanding available marketing choices and how they work is important for grain producers' bottom line and strategic planning. Entering harvest, corn producers have three primary choices of what to do with remaining bushels after fulfilling their pre-harvest corn contracts:

- selling off the combine,

- storing priced corn, and

- storing unpriced corn.

Each choice comes with benefits and costs. With any of the three choices farm constraints will influence the ultimate decision. These constraints are specific to each farm and consequently, left to the reader.

Selling off the combine is advisable if cash flow is required, storage is unavailable, returns to storage from storing priced corn for future delivery are negative and the outlook on future price expectations is not good (i.e., the wait-and-see approach). Returns to storage refers to financial benefits (or costs) from storage. However, when there appears to be a large crop, such as this year, positive returns to storage will likely exist, making choice No. 2 (storing priced corn) more attractive. Choice No. 3 (storing unpriced corn) is riskier than choice No. 2 because positive returns to storage will depend on factors influencing the futures market, which are out of the producer's control. Offering positive returns to storage is one of the four primary functions of a futures market. The other three are: price discovery, transfer price risk (hedging), and information dissemination.

Deciding to store corn, priced or unpriced, requires multiple considerations including futures market carry level, expected basis improvement between harvest and spring, cost of storage and spring corn futures price level expectations.

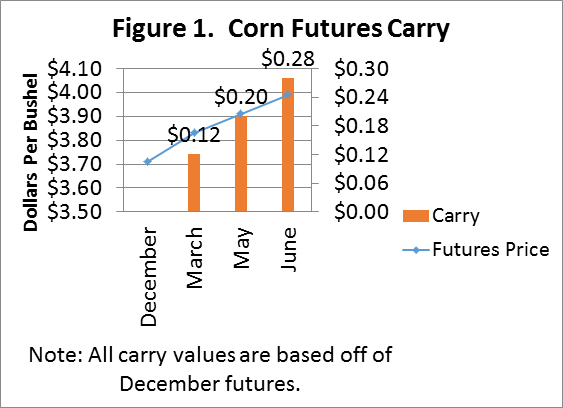

Carry

For any futures market commodity multiple contracts are being traded simultaneously. There are five contracts for corn: December, March, May, July, and September. The price difference between any two distant month futures contracts is called the carry and can be positive or negative (referred to as an inverted market). For example, during the first week of August this year, the December to May futures contract carry was $0.20 per bushel (Figure 1). In this case, the futures market is offering the producer $0.20 per bushel to store crop for delivery until May. To capture the $0.20 per bushel, the producer must sell the May futures contract, indicating they will store the commodity over winter and deliver grain in April.

Basis

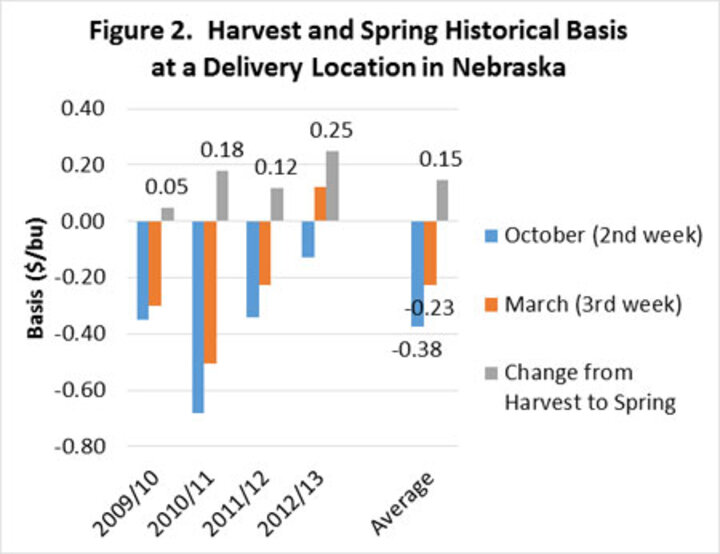

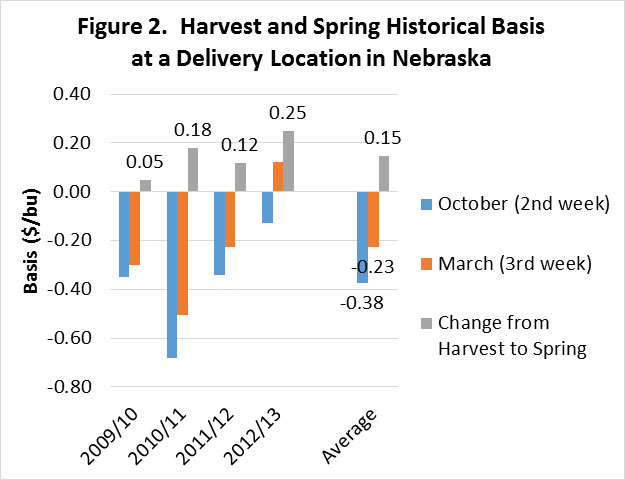

Along with the lowest futures prices of the year, harvest often brings the weakest basis. Using data from Extension Circular 846 "Nebraska Cash Corn Prices and Basis Patterns" (revision soon to be released), Figure 2 shows changes in basis values from harvest to spring for the past four years as well as the average basis for Beatrice. The basis improves an average of $0.15 per bushel from the second week of October to the third week in March. To accurately gauge local conditions, it is imperative to develop expected basis improvements between harvest and spring for each of the producer's potential delivery points. Once the grain has been sold for future delivery and quality is held constant, basis is the only remaining source of price risk.

Cost of Storage

It costs money to store grain and this cost must be accounted for when analyzing the decision to store corn. Cost of storage includes interest on the value of the stored crop, storage facility cost, drying cost, shrinkage cost, out-of-pocket storage costs such as handling costs, and insurance on stored product. If the cost of storage is greater than the carry and the expected basis increase, the market is signaling the producer to sell rather than store. Cost of storage is highly variable, depending upon producer specific variables such as storage facility type and location (on farm or in commercial storage) and consequently left to the reader.

Price Expectations

The final component in deciding whether to store priced or unpriced grain is spring corn futures price expectations (the wait-and-see approach). If you expect spring prices to rise higher than what the futures market is currently offering for a spring futures contract month, you may want to store unpriced grain. However, this is the riskiest option because prices could turn out to be unfavorable.

The cost of storage must be less than the gain in cash price for later delivery for corn being considered for a stored price strategy. The futures market carry is $0.20 between December and May. Expected basis gain is around $0.15. Thus, an additional $0.35 per bushel can be expected from corn priced for future delivery. The cost of storage would need to be less than $0.35 for a positive return to storage.

How do producers go about pricing grain for future delivery, given that positive returns to storage exist? Pricing grain for future delivery requires a number of steps.

- Determine when it is logical for you to deliver grain, who to deliver to, and when the carry plus expected increase in basis offers a benefit greater than the cost.

- Lock in the futures price around the time that grain is placed in storage. There are a couple of ways to lock a futures contract: take a short position through a personal brokerage account or, if you know who you will deliver grain to, sign a Hedge-to-Arrive (HTA) with the elevator. Both contract types lock in futures only, leaving basis open to change. Signing an HTA requires delivery to that elevator since they put up the margin money for you.

- Keep track of spring basis bids. Once a basis bid hits your expectations, sign a basis contract. Signing a basis contract with futures already locked provides the selling cash price.

- Deliver grain per basis contract rules. Throughout the storage period it is advisable to keep in good contact with your elevator for delivery.

This year it appears that storage priced for future delivery may be a viable, low-risk marketing option. The size of the expected returns from a storage priced strategy will vary daily based upon market factors. Consequently producers should keep a good eye on the markets. Basis will likely be very dynamic this year because of transportation issues, expected crop size, and variable storage capacity. Basis patterns after harvest will depend on the strength of demand.

Cory Walters, Extension Grain, Oilseed and Biofuels Economist

Jessica Johnson, Extension Educator, Panhandle REC, Scottsbluff